Obv the banks can fuck off, but I do seriously worry that we’ll see a response from banks regarding this, and it will probably be an increase in banks requiring your account to hold a minimum balance. They’re both pretty bad, so I’m not sure which is worse, but larger minimum balance requirements could push some people out of reach of a local bank account.

Being real a lot of people are skipping banks and just loading up visa gift cards and using those to buy stuff.

Most jobs require a bank account for direct deposit these days. Even pay cards are falling out of fashion. I spent a year working at a restaurant with a “i hate all taxes” libertarian owner and he still required all employees to set up a direct deposit. It keeps the books clean enough that any IRS audits wont come back demanding more money.

They’re skipping banks by using a ratshit solution that charges them between a flat $5 or 3% every month in fees…

Okay.

How much are your banking fees? In the UK almost all fees are £12.

Anywhere from $15 to $50+

Wow I wonder what the upper end is. We capped ours at that amount a good while ago now. When I worked at a couple of banks back in 08-14 they weren’t exactly new either.

Here’s some context for you.

For most of my life, banks ran an algorithm on overdrafting accounts so that charges would clear in whatever order triggered overdraft protection the most times. It was an open secret, then it came out and companies tried to insist they could do whatever they wanted.

Lots of real world cases of a single unexpected charge coming in and clearing a full day earlier than expected so a bunch of small charges (a pack of chewing gum) would each trigger the fee. $100 total charges, $500+ in overdraft fees.

Don’t transactions have timestamps? Or are you talking about paper cheques? Like I don’t trust the big banks in my country either, but I’m pretty sure all transactions are logged in real time and can’t be rearranged later.

Again, different countries might have banks work differently. When a debit is being applied (money removed from the account) it has a lifetime. First it is pending, and then it “clears”.

It clears when the bank approves that the money transfer is definitely happening, and that is the moment it is removed from your account. Importantly, the debit clearing from your account on a purchase does not mean the other party has fully received the money.

It used to be that a lot of charges would sit pending overnight and then all pending charges apply in the morning. Yes, even small purchases like a pack of gum bought at the corner store. All they did (and I think Wells Fargo in particular got caught and there were lawsuits about this) was decide the order of clearing pending charges with the intent of maximizing overdraft fees.

And how does that work? Let’s say I have $1000 in my account but forgot my $900 rent is coming out. ALong with some other transactions, they could clear like:

They could $0.99 gum, $150 car payment, $150 groceries, $900 rent. Overdraft fees = 1

Or

$900 rent, $150 car payment, $150 groceries, $0.99 gum. Same transactions processed at the same moment. Overdraft fees = 3! When that stuff happened to me back around '04, overdraft fees were $35 per overdraft. So that example was a $70 difference. In reality, between billpay and small purchases, the difference might be $500+.

My true story was that I had a dick of a landlord. My Bank’s autopay was running slow and despite the bank check already being in the mail and deducted from my account, my landlord insisted I pay immediately, and I was dumb enough to cave. So I cut him a check and asked him to hold it a day or two til the actual check was delivered; he cashed the same day. Double-rent for a 24 year older meant my account went into the red. I had 10 pending transactions (from gas to bill pays) for the next morning. All 10 (despite being already delivered and should’ve cleared first) waited to clear until the double-paid rent cleared. I was charged $350 in overdraft fees, almost as much as my $500 rent was (cheap back then lol). And despite agreeing the check getting to him late was their fault, my bank refused to refund more than $100 in overdraft fees because that’s what their algorithm valued my business at. I got the first rent payment back, fortunately. But was still out $250.

If I recall, the canned defense for this in lawsuits is “we just coincidentally process all transactions large to small instead of old to new because it makes sense to the bank to do so”. If I recall, some states (maybe fed?) ended up having to pass laws regulating overdraft fees a bit. It didn’t go far, but from what I hear it stopped that particular behavior.

This is very sad.

For us the transfer is either near-instantaneous (new system, called UPI) or done in batches every half an hour (old system). I guess this is why banks can’t do this trick.

I think it’s closer to that way now. There was incentive to banks in the past to process it differently.

That said, my bank’s “pay bills” function still takes your cash out before sending the check, despite the check NOT being a cashier’s check when not linked to an e-account. They just refund you in 90 days (or so) if it isn’t cashed.

Very interesting.

As far as I’m aware most normal banks here don’t have overdraft fees, they just charge interest for every day you spend in the overdraft. Depending how deep you are in it (as long as it is an agreed overdraft) then it could end up being pennies to a couple of pound maybe.

A non agreed overdraft I believe will incur a fee plus the interest per day perhaps at a higher rate. I’m not sure but I think it’s a single fee a day (as in if something comes out that’s a £12 fee, if you remain in overdraft but no further withdrawals/charges then no more fees) but don’t quote me on that. It’s been a very long time since I was in an overdraft and longer since I worked in a bank!

what the upper end is

“Lol” said the US banks, “LMAO”

Well, you can trigger multiple in a day, so you can get a couple hundred or more if the stars align right.

Eesh

deleted by creator

Something something most of Europe does not allow you to overdraft your account and people get by just fine something

I don’t see the issue with overdrafting, just why the hell do you guys have a flat fee for it instead of just exorbitant interest rates? Even 50% interest doesn’t cost much if it’s for overdrafting a few hundred for 3 days because i lost track of how much money is in my main bank account.

The one time overdrafting cost me anything close to significant money is when I thought my account had overdrafting allowed but then my bank reverted a transaction because apparently all previous instances were just them “tolerating it”. My PC died and I wanted a new one asap, but the money for that was on my savings account, so I figured I’d just go to like -300 for 1 or 2 days. Nope, bank takes the money back, amazon makes me pay like 20€ of fees, and I have to deal with the bureaucracy of it all. At least I got my PC parts quickly anyway.

Overdrafting with a sane system is just even more expensive credit card debt.

But clearly you guys have less freedom than Americans, because that’s what American TV told me.

That heavily depends on the country, but in general you have to ask for permission rather than forgiveness.

The right to be exploited is sacred to us!

people get by just fine

debatable but otherwise the point stands.

A lot of US banks also have that as an option, people opt in to “overdraft protection” anyway. The banks make it sound like a safer option, instead of the predatory practice it normally is.

I’ve had them turn it off, and then one day they just… Did it again. Bastards don’t even respect that because they think they know better.

Many banks straight up do not allow you to turn off overdraft protection. The bank I had before moving to a credit union did that.

Checked what else she has written, the next article along was seriously “How far should we be willing to go to silence Nazis?”

She’s worried that if Nazi’s can’t have their free speech then they’ll come for the white supremacists who don’t identify as Nazis next…and that apparently sets a very dangerous precedent!!

This is a weird topic, because on the one hand, they have every right to speak and assemble, no matter how much we like it. Even the ACLU took on a case defending the American Nazi Party and their right to assemble and march. It truly is a right which the government cannot have any say in who it applies to. I won’t go into any bullshit argument that they’ll go after other people next, but it’s a right that needs to apply to everyone.

However, that only applies to the government. Everyone else can and should tell them to go fuck themselves and corporations can ban their asses from every service online. They don’t have any right to having their voices amplified online or any other service.

If you support rights you end up spending your entire life defending the worse example of those rights put to use.

First they came for the Nazis, and I didn’t speak up, for I wasn’t a Nazi.

Then they came for the white nationalists, and I didn’t speak up for I wasn’t a white nationalist.

Then they came for the fascist insurrectionists, and I didn’t speak up for I wasn’t a fascist insurrectionist.

Then noone came for me because I wasn’t a fucking monster, and by that time, there was no monsters left to whine about culture war bullshit.

Then the country was pretty damn great, actually, and we enjoyed our new found freedom and age of equality and prosperity.

When we start rounding up nazi’s and white supremacists, I will absolutely speak up! I will be waving flags and walking the street. I will be shouting and going to gatherings where people will be shouting. And the shouting will sound something like “woohoo!”

The “slippery slope” logical fallacy. A classic tool in the braindead conservative debate kit.

No, it’s not inherently a fallacy. Case in point, the Patriot Act and everything that followed.

Yes, it can be used to support idiotic arguments like that legalizing gay marriage will lead to beastiality, or anything that Megan McArdle will use it to support, but it shouldn’t be automatically dismissed as an invalid concern.

I kinda of get where the concern comes from and I am very much not a conservative.

My concern with censorship is that if we instrument a legal way for the government to force media (social or otherwise) to suppress a point of view, that it will be later used against us.

It’s great if we want to silence Nazis, but I feel that the US is dangerously close to being taken over by Nazis! I think Trump has a legit chance of winning (hopefully he is not allowed to run based on the insurrection clause) and I can definitely see GOP getting legislative majority too. I don’t like to think about a MAGA controlled government having the ability to control the discourse of the people…

But obviously, things would be better without all the hate and disinformation being spread like it currently is. MAGA and qanon and all that authoritarian bullshit really is like a mind virus…

I dont have a solution, but I don’t think censorship is worth the risk. I guess all we can do is continue to socially stigmatize hateful speech and disinformation.

My concern with censorship is that if we instrument a legal way for the government to force media (social or otherwise) to suppress a point of view, that it will be later used against us.

It absolutely will. Any mechanism of authority will be abused later for things unrelated to its original purpose. We need to undo authoritarian control and spend all that money on education then stand back let society decide on its own without coercion. Think of this.

At one time the government felt the need to do something about actual snake oil salesmen. And conservatives at the time were like “It’s crazy to let the government tell you what to eat drink.” But progressives were like “No we gotta put people in jail.” Fast forward less than 100 years and large segments of the population become disenfranchised for smoking a dry plant in private on their own land.

Everything the FDA does should be about providing information, education, recommendation, grading purity and so on. “This soda contains 5 mg of cocaine as certified by the FDA inspection.” And starting in fifth grade every kid gets fact-based info on what drugs do.

The solution to absolute free speech is mandatory and repeated education on critical thinking, logical fallacies, propaganda techniques and cognitive biases. I recall propaganda techniques being discussed in fifth grade in the mid 70s.

Has anyone stopped to consider that maybe she’s just a ragebait shill? and everyone angry about her and talking about her are doing exactly as she intended. Occupying your brain space and wasting your time, distracting you from a million more important things you could be doing.

Even if that’s true, she should be posting on 4chan not Washington Post.

Exactly. That’s why I say she’s a shill. Shills earn good money from some invisible upper authority to write this shit. For example David Icke is another shill of a different flavor.

You know, if AT&T starts shutting off phone service to people who repeatedly talk about how Hitler made good points, I won’t lose any sleep over it. If I know better than to talk about how burning down billboards is based via SMS, then nazis should know better than to talk about how cool Hitler was.

I also love how she says that “conservative Christians” are being targeted too, and the two links she provides are about a church that “offers help to people who want to move away from same-sex attraction or behaviours,” aka conversion therapy, aka a practice that’s been proven ineffective and harmful, and a story about Vanco dropping the Ruth Institute for “promoting hate.” But they don’t promote hate! All they do (literally all they do) is try to destroy the rights of LGBT folks! You name something the LGBT community likes, the Ruth Institute has probably spent time and energy fighting against it.

If conservative Christians are all like the Ruth Institute and Core Issues Trust, then I say cancel em all.

Well they sound like a fun group.

“you are bad and should not exist and should not love who you want or have a family” … “It just so happens we are able to cure you by changing you into something else, thus redeeming you in our eyes!”

I know this is basically religion 101, but screw them just the same.

Under very, very limited circumstances, maybe. Like you need gas to get to work now, get paid tomorrow, and have nothing in your account? Yeah, maybe, but that’s an expensive tank of gas for someone that’s that short on cash.

OTOH, I can’t count the number of times where my former bank processed my paycheck last–even though it went in first–and then hit me with overdraft fees for buying groceries, gas, paying bills, etc. (This was National City Bank; they ended up losing a class action lawsuit about it, but they still made more money from their theft than they had to pay back out.)

IMO, there should be zero overdraft fees; if the money isn’t in your account, the charge is declined. All of this shit should be done in real-time, instead of waiting for a merchant to post at the end of the day. This is the twenty-fucking-second century, and it’s not that goddamn hard.

Or even better, make banks immediately start treating any negative balance as a credit. There can be a low limit, but enforce a low interest rate. For all that banks have done to us, I feel like this is literally the least they can do—and shit, they’d still turn more profit.

This is actually not a terrible idea. Though interest rates in general need to be capped on lines of credit of all varieties. The fact that 45% interest on a credit card is not being brought up on usury charges is insane.

Upsetting to hear banks don’t get any better a century from now. Good luck to you future man.

What’s funny is that it looked odd when I read it, but I just quickly brushed it off as a “well you don’t see it written often.”

You can disable overdraft “protection” at many banks. I disabled it on my account when Commerce Bank got eaten by TD, and they transferred years of withdrawls then deposits to “balance” my account between systems and I was handed a potential few-thousand-dollar overdraft pile. Told them to kiss the fattest part of my ass and disable overdraft immediately.

Ive had overdraft off on my account since i opened it. However theres been a few things that still are allowed. My truck note is one of them, and state/federal/irs stuff im told would likely be allowed too. I once double paid my truck not on accident, and that was a fun trip to the bank to put a stop payment in.

IIRC part of the problem is that merchants don’t necessarily post charges to your account immediately. They place a hold on funds, but it’s not necessarily charged. That’s especially true for buying gas, where the amount you are going to spend isn’t known until after you’re done filling your tank. The way around that is to have to pre-pay for gas.

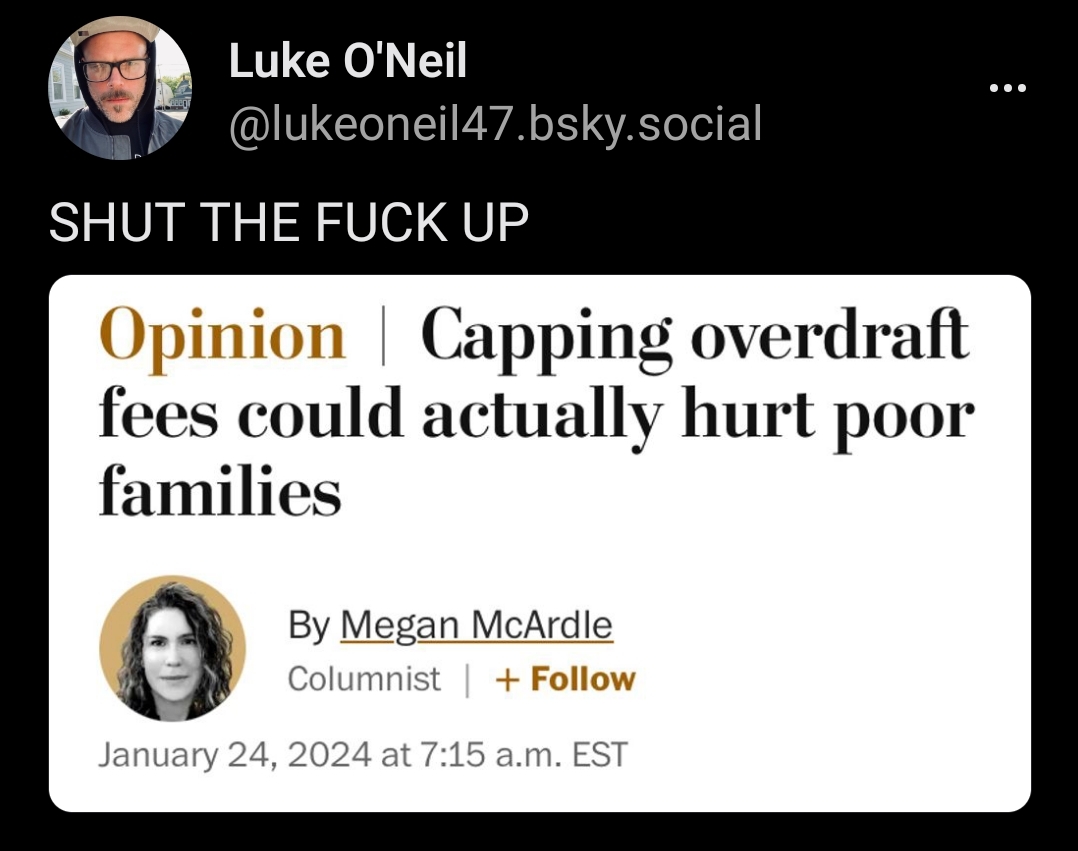

Megan is a national treasure.

You can always count on her to selflessly use her to name to publish the most absurdly dog shit arguments to defend corporations and the powerful.

She’s also pretty dumb.

She’s also pretty dumb.

is she or does she just know where her paycheck is coming from?

That’s a question you’d only ask if you haven’t read any of her writing…

Might I suggest starting with her pieces on The Handmaid’s Tale, the Grenfell Tower Fire, and anything to do with kitchenware.

If we cap overdraft fees, how will banks make up the lost revenue?

Get in the fucking sea.

I wonder if banks could try lending money to companies and charging a fee for this service. Like some sorta investing + banking system. Hmmm

Opinion: removing water from the world could solve world thirst

There are definitely scenarios where the ability to temporarily overdraft an account saves people much bigger missed payment fees and interest charges.

I don’t know why we can’t just have the fees come on a deferred basis. Like if your account returns to positive within the billing cycle then the fees get waived. No reason they need to be predatory

I don’t know why we can’t just have the fees come on a deferred basis

The other guy already said it but I’m going to reiterate for emphasis:

Banks are not your friends. Banks (in the US) exist as for-profit businesses to make money off of you

Edit for clarity: The main way banks make money off of you is by investing the actual cash you give them and agreeing to cover your day to day costs of living. Since the vast majority of people prefer to have a positive bank balance and possibly a savings, it works out that the banks always have money to invest.

It stands to reason that anyone with a negative balance is actively infringing their strategy to invest excess money, so why wouldn’t they charge them? It’s all business.

Because I would imagine that the banks don’t want to give a small interest free loan in that scenario? With no collateral on a regular recurring basis that one day will never be paid off?

Not that I feel bad for the banks…

Note: I’ve turned overdraft off with every account I’ve ever used and I don’t use Auto pay because you gotta be strategic sometimes.

Megan McArdle is the dumbest bitch in the world. I refuse to click on anything she writes because her shitty takes don’t deserve views. She’s actually a big part of why I unsubscribed from WaPo (that and the whole neolib vibe) because I want zero of my dollars benefiting her.

I have no desire to read but I bet her argument comes down to “if they don’t have overdraft fees then they will go into deeper debt by overdrafting more and that is worse somehow”

So the argument is essentially if the poor don’t have overdraft fees, someone else like the middle class will have more fees?

Usually the defense behind banks ‘allowing’ overdrafting is that surely you wouldn’t want to miss paying a bill because your paycheck hasn’t landed yet. So the argument here would probably be if you cap overdraft fees, then banks won’t allow overdrafting anymore and then poor families will have their electricity shut off and get evicted.

All the extra debt they get could have been bank fees, why don’t you think of the starving CEO’s, else they can’t afford their Beluga Caviar and Dom Pérignon dinners.

Megan McArdle is the dumbest bitch in the world.

Grandma Lauren Boebert exists, you know

You know what, let’s just go ahead and say there are many, many dumb bitches (men included) in the Republican party who are constantly fighting for the crown.

I cancelled my wapo subscription over similar. Glad to be rid of them honestly.

deleted by creator

well, duh. Your Bank will just stop allowing you to overdraft, declining your Transactions.

I have never ever had a transaction that overdrafted where I was happy they didn’t just decline it. Zero desire to pay $38 for the “convenience” when I could have just used a different card.

I’ve asked my bank to not allow it on my account at all and they told me NO, they can’t do that, because it’s “a service we provide our customers for their convenience”. Right. I don’t want that convenience, dicks.

Goooood! No more free money from broke people. Go get a court to force them to pay!

deleted by creator

It’s even more fun when they transfer from your savings account to cover the overdraft and charge you the overdraft fee anyways.

I encountered this enough with my CU; after kicking my college-induced points-fueled credit card habit; that I just decided to switch to a fee-free checking account with capital one. Physical branch locations be damned.

I could only tolerate so many multiple $3 charges a day, with no specific notification, for a service (a savings transfer) that would be completely free if I were to initiate it. And then “we can refund up to 3 overdraft charges but you should monitor your accounts more closely”. lol. Keep your $9 and shove it, I shouldn’t have to babysit my fucking credit union to keep their hands out of my pockets as I’m going through a major life transition like this.

Anyways. Capital one’s verification process has been a bit of a headache but I’m currently trusting the process.

A couple decades ago I opted out of overdraft protection for this very reason, so the bank would just reject the charges, and then hit me with a $36 fee anyways. Fucking criminals.

Yup, this is how overdraft protection works at my bank too. Like, what costs money in just saying “transaction declined”? It’s not like the banks owe money to themselves on an OD account.

Overdraft is optional on every account I’ve had tbh.

It ought to be defaulted to Off.

I’ve turned it off every time but I have to ask every time. They don’t even tell you it’s default to on cause they wanna collect the fees.

Yeah stop talking about corpos like they’re forces of nature or phenomena . “Oh if the bank no money then no loans or whatever” nah that’s a choice. Made by people. People with cars that can be keyed. Allegedly.

{kind=link}