My salary didn’t change at all, but homes went up 82%. The money I saved for a down payment and my salary no longer are good enough for this home and many others. This ain’t even a “good” home either. It was a 200k meh average ok home before. Now it’s simply unaffordable

You must log in or register to comment.

:laughs in Australian:

House down the st was 94k in 2015, it sold for 195500 last year.

What I’m hearing is that houses have the ability to be a great investment.

Work to get a house and then when you are old and ready to retire you sell and then have a great retirement.

…until you realize that you still need a place to live after retirement, and any house you’re buying will have the same average increase across the board.

I’m talking much later in life when some of the basic things become a little harder but still doable. You move into an apartment that is for older folks.

Where tf do you live then? You’re just gonna need to buy another home

You downsize to a small apartment for older folks.

Those cost more than a house! The one my friends dad lived in where it was all in the same building and the staff was there just in case you fell was 4k a month.

It depends on where you go. You probably don’t need much in terms of space and features.

Bought our cottage for 50k at the peak of the rural movement in 2020 after it had been on the market for months, just sold it while the second property market has completely crashed for 130k after putting 10k in it and cleaning the fuck out of the lot (the place was disgusting, I’m talking 90 industrial garbage bags of crap, mostly beer bottles, a couple tons of wood and concrete and so on)…

Sometimes you’re just lucky and people don’t want to do what’s required to get what their property is worth!

Real talk, forget about a down payment. There are a bunch of different ways to get a 0 down mortgage with varying qualifiers so that chances you qualify for one of them is quite decent.

Even if not, there are still a bunch of other ways to get low down payment mortgages for ~3% down or less.

Toss out the old adage of “20% down or bust” and keep any money saved towards it for savings for all the other costs of home/closing

This is terrible advice. Paying anything you can up front saves you several times over in the long run.

Let’s talk 500k house, 6%, 30 years, no pmi, no taxes, no extras…

Paying 100k (20%) up front you’ll pay: $863,352.76

Paying 50k (10%) up front you’ll pay: $971,271.85

Paying 0 up front you’ll pay: $1,079,190.95Paying 20% down (100k) will save you over 200k.

If you intend to live in the house indefinitely, you’re so much better off if you put as much into the down payment as you can.

Edit: List formatting

That’s great, in theory. In reality, you’ll get stuck in a perpetual savings cycle like OP and in many cases never reach the mythical threshold.

200k savings sounds nice, but if you have to spend 5 years saving and housing prices jump 80, 90, 200% in that time that savings lead gets entirely erased.

You can always play around with your interest rate later on, but you can never change what you paid for the house

housing prices jump 80, 90, 200%

Happened once and we are currently dealing with the consequences., tbd

Also pay on time and as much as you can. Don’t fall into the trap of paying to close to or at the minimum. If you do that you will be in loads of dept.

The longer you wait to pay something off the more interest it gains.

This is terrible advice. Paying anything you can up front saves you several times over in the long run.

Usually, yes, but it’s situational.

For example, I bought my house in 2009 during the depths of the Great Recession, with no down payment, and got a screaming deal. If I had decided to wait a few years to save up for a down payment, I would’ve been 500% screwed.

(That “500%” isn’t hyperbole, by the way: that’s how much more I would’ve had to spend to buy my house now instead of back then! Actually, I’d have been even more screwed than that, considering that I’d be paying ever-increasing rent the whole time, too.)

This presumes you can elect to either just spend the 100k now, that you may not have.

If you declare you want 100k, but let’s say that would take you 10 years (and the goalposts wil move). That’s likely 120 months of rent you will have to pay, so while you’ll end up saving on interest, you’ll more than lose out on rent.

Paying down aggressively and going with as big a down payment as you can reasonably afford makes sense. However waiting to save up for that downpayment may cost more in rental expenses than you’d save.

Good thing what I actually said was

Paying anything you can up front saves you several times over in the long run.

My point was that the advice was terrible. Not that there are other circumstances that could make it useful. Overall, as a general rule you shouldn’t want to just hold onto debt for no reason if you have means to pay it down. It’s also why I specifically showed 10% as well rather than just the typical 20% downpayment, it furthers my point that

you’re so much better off if you put as much into the down payment as you can.

“As much […] as you can” And not just some 20% or whatever magic number.

While true, I was thinking more about how the person you replying to probably was reacting to the trend of people talking about saving and waiting until they had a reasonable downpayment before they would consider entering the market, and how the market keeps running away from their downpayment savings.

The ‘never make a downpayment regardless of context’ would be bad advice, but I just presume there is a context in mind about not even having the downpayment to start with and being stuck on the rental treadmill as a result.

What income to loan ratio are you talking here?

Not that this is “ok” but it’s why “buy whatever you can as soon as you can” is good advice. If you’d put whatever you had into a shitty condo four years ago, and kept saving at the same rate, you’d likely be in good position to trade up soon.

I see a lot of people I know end up in the same position because they’ve been waiting for either the exact right circumstances or for prices to “crash.” All the people i know who started with anything they could afford now have a huge amount of equity in nice homes. The difference is real and primarily about timing more than income or location.

I bought 5 years ago when it was still reasonable. I have a great rate on a great house that has increased by about 50% since I bought it.

I don’t want to, because this is just about the perfect size house for us in a great location, but I can’t really “trade up” as the interest rates are through the roof and everything is more expensive too.

If your circumstances change, you can make a lateral move and invest the net profit in an index fund.

I think you misunderstand. He didn’t have the financial wherewithal to acquire a home of any sort because a down payment was expected even of the shitty condo. He didn’t have the money then he doesn’t have the money now he’s on the same shitty treadmill that the rest of us in the permanent underclass are.

Y’all realize this is a bubble, right? I almost feel sorry for these investors, gonna have their ass handed to them in the coming decade.

If Big Macs, houses, gas and college tuition all went up, it’s time to realize these are not all in bubbles and instead realize due to inflation your salary has been halved.

No true! Plebs got 12% raises over last few years ans even for one quarter outpaced inflation 🤡

Y’all realize this is a bubble, right?

Can you explain why you feel that way?

I feel sorry for any one whose bought a house over the last couple years.

Bought a house 5 years ago. Cheaper than renting and equity says I made 100k. It’s good.

It’s just lame how expensive they are now. BTW, they were to expensive 5 years ago too.

I don’t, it’s strictly better than renting

Is it though? My understanding is it’s more complicated than “simply better”. You need to account for property tax, home repairs, lack of mobility, housing market, etc.

It’s more along the lines of “buying is generally better than renting, but there are about 100 different factors to consider.”

My mortgage is significantly less than my last apartment down the road. $2700 vs $2100. Same size living space (1000sqft, 2bed), an extra basement, and I get to live in a marginally more affluent area. That difference in monthly payments more than covers monthly housing maintenance costs. And property tax is already included in that $2100 mortgage, which is how it is usually handled in my state.

And you get equity instead of throwing away your income to a faceless real estate corporation for no gain. Owning a house is 100% better in every way, unless you need to quickly move for some reason.

But even then, it’s rare to see a house be on the market for more than a month, MAYBE two before getting sold. You can move out on a couple months notice, instead of having to wait for your annual lease to run out.

But when you do move, you sell your house for ✨ profit ✨ because the housing market only goes UP for some retarded reason.

I’ve helped three friends and coworkers navigate buying their first house in the past couple years. They are all better off financially for it.

The main downside is you have to pay closing costs to move. That means you should plan to stay in the home at least a handful of years or else you’d lose money likely. But with the market the way it is, get a house ASAP cause its going up like a roller coaster.

I bought mine 5 years ago and its gone up 50% in value since then.

There are advantages I’m not actually culpable for all of the maintenance of my property my actual rent right now is just about on par with anybody who is going to be paying to purchase their house and granted I’m not actually gaining anything as far as property value I also didn’t have to come up with a down payment or jump through hoops and try and get the house in the first place and very safe in my position and I’m very capable at this point after having lived here for many years landlord hasn’t asked for a new lease in the last couple years so I could actually walk away at any moment… there are benefits but they’re few

The rental aspect isn’t a bubble. Until they start viciously taxing single-family home rental, home prices are going to stay high because they’re not being bought as homes but as assets for rent-seeking.

Not really. The system will instead keep finding ways to get people to rent at higher prices or take out low down payment loans with ever larger monthly payments taking a lot more of take home salaries and making it harder than ever to save and invest.

Shout out to [email protected]

It depends on the area. Some places are actually gowning that fast in population

That’s cheap as hell compared to California. And I work remote from anywhere I want. Thanks for the tip!

Also here in Europe this is the type of construction we use for a garden shed, not a house.

Even when we do modern timber frame, it’s generally still brick or block at the bottom. How long do these houses last in the US? I imagine a lot of the continent is pretty humid

My parents’ timber house is from the 1780s and is still solid. So, 240 years at least, give or take. I’m aware of plenty of timber houses from the 1600s that are still standing and functional as well.

Is a timber frame house from back then the same as one built post 1950 though? Some Q’s:

- Have materials/practices decreased in quality?

- Has there been a shift from a sense of pride in craft and duty to build well towards cutting corners and saving $?

- Has the density and properties of wood changed as we use smaller trees grown more quickly in monocultures compared to old-growth harvested lumber of pre 1900s?

Well, the house I’m living in now was built in the 1960s, and is also still very solid.

When wood is properly sealed up in walls, it lasts a very long time. We don’t really have buildings on an old world timescale, but we do still have colonial wood frame buildings.

Timber frames are sheathed in treated plywood and then wrapped in siding. Rain doesn’t reach the wood of a barely-maintained house, exterior humidity won’t do damage in any hurry, and wood is rarely making ground contact. These houses last at least a hundred years given that this style is approaching 100 years. It’s usually storm damage through the roof that causes the rotted wood you’re imagining, not normal wear and tear.

It’s a good thing you aren’t a building engineer.

In California at least, houses made with a wooden frame are usually on top of concrete (either a concrete slab under the whole house, or a concrete perimeter under the exterior walls), and the frame is bolted into the concrete along the entire perimeter.

Older homes often aren’t bolted into the concrete, but it’s common to retrofit this to improve earthquake resistance. Without the bolting, the house can move around during an earthquake. The government here has a program (Earthquake Brace and Bolt) where they cover part of the cost of doing this work.

Masonry (houses made of bricks, stone, etc) are much less common here, since they perform much worse in earthquakes.

👍 in Europe earthquakes luckily are less of a concern, so we care more about longevity (you’ll find many places where pretty much every house is well over a hundred years old (the oldest one in my village is about 900 years old)) and good isolation (to keep the heat inside in winter and outside in summer so we can heat less / don’t have to use air conditioning on our way to net zero)

Time to eat the rich

Best hurry … Ozempic is destroying the caloric benefit

No rich person is living in a 325k ranch house.

My man let me introduce you to globalism and people living in refugee camps in South Sudan.

$325K is more money than most of the people in the world for all of history would see in a lifetime.

Wake up to your riches.

If the house hasn’t changed, then the value is basically the same.

The price change is more about how rapidly the USD is devaluing.

Between 2020 and 2024 there was about 22% inflation. 1.22x$195,400=$238,388. So there’s still over $110,000 of price inflation to account for past devaluation of the dollar.

there was about 22% inflation

I’m not disagreeing with you, but I just wanted to note that inflation numbers (more specifically, the CPI) is an average across multiple industries - supermarkets, rent/mortgage, furniture, cars, flights, health care, and several more. It’s possible for inflation to affect some industries much more than others and I wouldn’t expect everything to all go up at the same rate.

That’s true and worth noting. The difference is much starker when the benchmark is food and fuel, since real estate (and stocks) rose much higher compared to other things.

Houses in my neighborhood are up 150-200%.

So occasionally I look out of curiosity and the reason is pretty plain.

I look for houses for sale in a suburban area as public listings, and there’s like 1 within a few square miles of the area.

I switch over to renting, and there’s like 12 houses just like the one for sale available, all owned by companies. I also know a coule that aren’t listed that have no tenants, but are still owned by one of those companies. You can tell because those yards are now waist deep grasses (in an area where HOA throws a hissy fit if your yard looks just a smidge unkempt).

Don’t know why the companies find it more profitable to buy houses people aren’t looking to actually move into, at least at the rent they are willing to accept. If I fully understood why, it might just piss me off more. Like maybe the houses work better as a loan basis than other assets, so even empty and unused they are valuable as some sort of financial trick.

My understanding is that these companies are investment companies that need stable assets for their billions of dollars portfolios and they actively look to keep buying property as a stable form of appreciating asset. They have so much money that needs to find some way to make more money for their investors.

Don’t know why the companies find it more profitable to buy houses people aren’t looking to actually move into, at least at the rent they are willing to accept. If I fully understood why, it might just piss me off more. Like maybe the houses work better as a loan basis than other assets, so even empty and unused they are valuable as some sort of financial trick.

That’s one thing, but housing has been a low-risk investment for a long, long time. If they bought the house OP posted in 2020 and sold it in 2024 they would have almost doubled their money even without renting it out.

I like the utility feed hanging off the front of the house going straight through the roof and blocking them from installing the other fake shutter. I wonder what other construction horrors lurk inside.

Has the population jumped up for ya guys?

Don’t know about them specifically, but it seems that more than anything real estate investors are just grabbing as many properties as they can find, whether they can get tenants or not. A house goes up for sale and it’s bought sight unseen by a company almost instantly.

That’s crazy

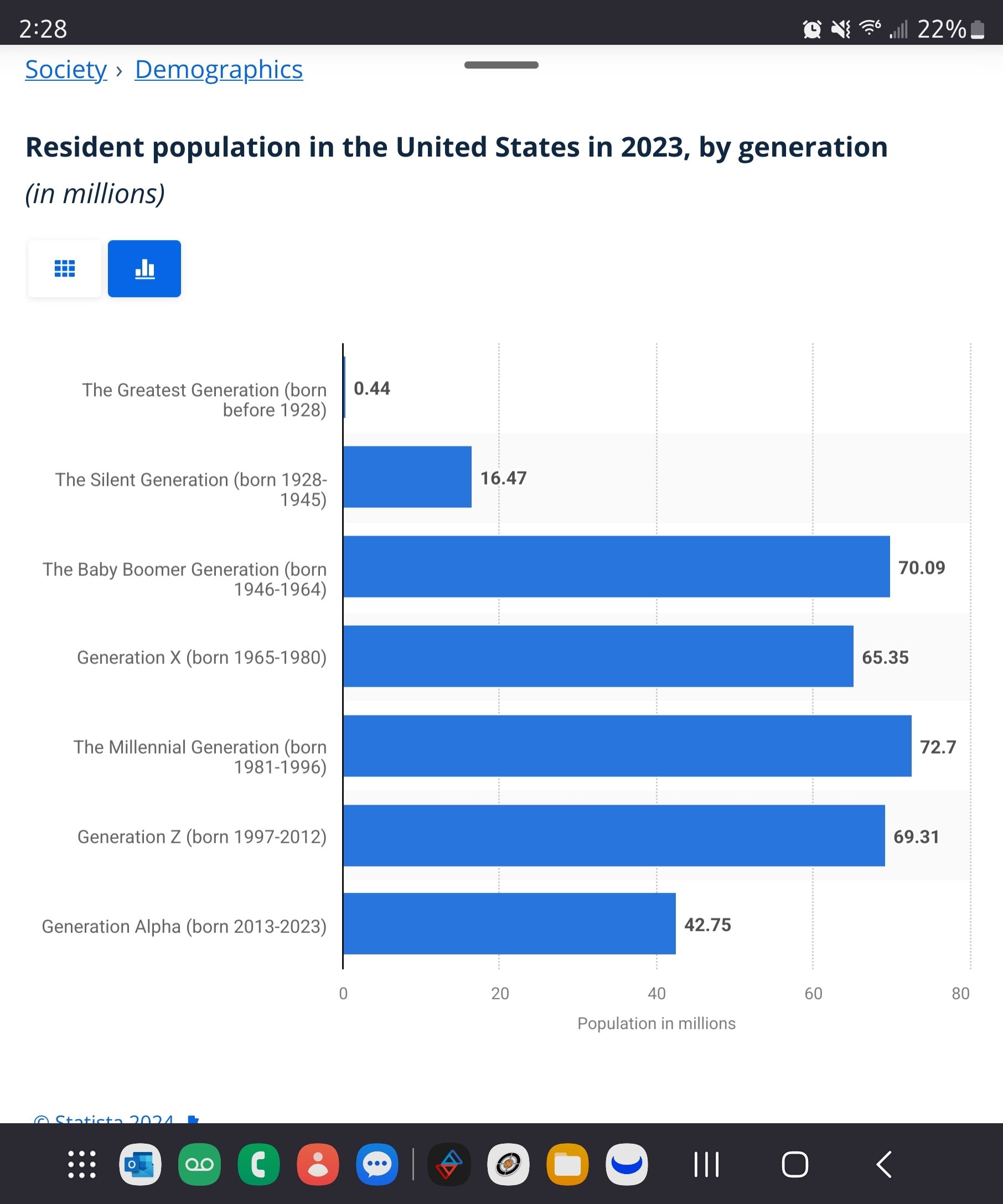

Yes the largest generational share of the population is the millennials most of whom are just becoming the age of the average first time homebuyer. Creating a sharp spike in demand for realestate.

Ya but does that happen with every generation then? Having a sharp spike of first time homebuyers.

Most millennials would be buying homes already. The end of the millennial group is coming up on 30 so I wouldn’t expect them to be the driving force for first time buyers when so many are already established

I’ll have to look it up to he sure but I wanna say millenials were the largest population increase for a generation since the boomers. Which would make up the really close to the entire existence of the eealestate market as we know it. Wanna say 1930’s the new deal created the foundation of the modern mortgage loan. Either way, the answer is no it does not go up for every generational transition.

It’s actually only the second time it has and will go up by the time gen z cycles to home buying in a span longer than 150 years.

I wanna say you were thinking of this in terms of total population growth increasing but it really is more of a combo between birth rate and poulation percent change, except instead of year over year it is 15 year wondow over 15 year window or however long each generational span is.

Yep, that’s on track! My house has almost tripled in price since I bought it 12 years ago. Denver metro. No way I could afford it if I had to buy it today.

Houses only increased a little bit. The rest is inflation making your salary 30% less

A little bit… Bahaha Hahaha ya ok guy. Just a little bit

{kind=link}